Islamic Banking Definition: History and activities

What

Is Islamic Banking?

Islamic banking, also referred to as Islamic finance or

Shariah-compliant finance, refers to financial activities that adhere to Shariah

(Islamic law). Two fundamental principles of Islamic banking are the sharing of

profit and loss and the prohibition of the collection and payment of interest

by lenders and investors

KEY TAKEAWAYS

- 1. Islamic banking, also referred to as Islamic finance or Shariah-compliant finance, refers to finance or banking activities that adhere to Shariah (Islamic law).

- 2. Two fundamental principles of Islamic banking are the sharing of profit and loss and the prohibition of the collection and payment of interest by lenders and investors.

- 3. Islamic banks make a profit through equity participation, which requires a borrower to give the bank a share in their profits rather than paying interest.

- 4. Some conventional banks have windows or sections that provide designated Islamic banking services to their customers.

Understanding Islamic Banking Practices

There are approximately 520 banks and 1,700 mutual funds

around the world that comply with Islamic principles. Between 2012 and 2019,

Islamic financial assets grew from $1.7 trillion to $2.8 trillion and are

projected to grow to nearly $3.7 trillion by 2024, according to a 2020 report

by the Islamic Corporation for the Development of Private Sector (ICD) and

Refinitiv. This growth is largely due to the rising economies of Muslim

countries (especially those that have benefited from oil price increases).

The anticipated growth of the global Islamic finance

industry from 2021 to 2022 is due to increased bond issuance and a continuing

economic recovery in the financial markets, according to S&P Global

Ratings. Islamic assets did manage to expand by over 10% in 2020, despite the

COVID-19 pandemic.

Islamic banking is grounded in the tenets of the Islamic

faith as they relate to commercial transactions. The principles of Islamic

banking are derived from the Quran–the central religious text of Islam. In

Islamic banking, all transactions must comply with Shariah, the legal code of

Islam (based on the teachings of the Quran). The rules that govern commercial

transactions in Islamic banking are referred to as fiqh al-muamalat.

Employees of institutions that abide by Islamic banking are

trusted to not deviate from the fundamental principles of the Quran while they

are conducting business. When more information or guidance is necessary,

Islamic bankers turn to learned scholars or use independent reasoning based on

scholarship and customary practices.

One of the primary differences between conventional banking

systems and Islamic banking is that Islamic banking prohibits usury and

speculation. Shariah strictly prohibits any form of speculation or gambling,

which is referred to as maisir. Shariah also prohibits taking interest on

loans. In addition, any investments involving items or substances that are

prohibited in the Quran—including alcohol, gambling, and pork—are also

prohibited. In this way, Islamic banking can be considered a culturally

distinct form of ethical investing.

To earn money without the typical practice of charging interest,

Islamic banks use equity participation systems. Equity participation means if a

bank loans money to a business, the business will pay back the loan without

interest and instead give the bank a share in its profits. If the business

defaults or does not earn a profit, then the bank also does not benefit. In

general, Islamic banking institutions tend to be more risk-averse in their

investment practices. As a result, they typically avoid businesses that could be

associated with economic bubbles.

An Islamic bank is entirely operated using Islamic principles, while an Islamic window refers to services that are based on Islamic principles that are provided by a conventional bank. Some commercial banks offer Islamic banking services through dedicated windows or sections.

RIBA and Profit

The practices of Islamic banking are usually traced back to

businesspeople in the Middle East who started engaging in financial

transactions with their European counterparts during the Medieval era. At

first, they used the same financial principles as the Europeans. However, over

time, as trading systems developed and European countries started establishing

local branches of their banks in the Middle East, some of these banks adopted

the local customs of the region where they were newly established, primarily

no-interest financial systems that worked on a profit-and-loss sharing method.

By adopting these practices, these European banks could also serve the needs of

local businesspeople who were Muslim.

Beginning in the 1960s, Islamic banking resurfaced in the

modern world, and since 1975, many new interest-free banks have opened. Though

the majority of these institutions were founded in Muslim countries, Islamic

banks also opened in Western Europe during the early 1980s. In addition,

national interest-free banking systems have been developed by the governments

of Iran, Sudan, and (to a lesser extent) Pakistan.

Example of Islamic Banking

The Mit-Ghamr Savings Bank, established in 1963 in Egypt, is

commonly referred to as the first example of Islamic banking in the modern

world. When Mit-Ghamr loaned money to businesses, it did so based on a

profit-sharing model. The Mit-Ghamr project was closed in 1967 due to political

factors, but during its year of operations, the bank exercised a great deal of

caution, only approving about 40% of its business loan applications. However,

in economically good times, the bank's default ratio was said to be zero.

The primary objective of establishing Islamic banks all over

the world is to promote, foster, and develop the application of Islamic

principles in the business sector. More specifically, the objectives of Islamic

banking when viewed in the context of its role in the economy are listed as

follows:

- · To offer contemporary financial services in conformity with Islamic Shariah;

- · To contribute towards economic development and prosperity within the principles of Islamic justice;

- · Optimum allocation of scarce financial resources; and

- · To help ensure equitable distribution of income.

These objectives are discussed below.

- Offer Financial Services: Interest-based banking, which is considered a practice of Riba in financial transactions, is unanimously identified as anti-Islamic. That means all transactions made under conventional banking are unlawful according to Islamic Shariah. Thus, the emergence of Islamic banking is clearly intended to provide for Shariah-approved financial transactions.

- Islamic Banking for Development: Islamic banking is claimed to be more development-oriented than its conventional counterpart. The concept of profit sharing is a built-in development promoter since it establishes a direct relationship between the bank's return on investment and the successful operation of the business by the entrepreneurs.

- Optimum Allocation of Resources: Another important objective of Islamic banking is the optimum allocation of scarce resources. The foundation of the Islamic banking system is that it promotes the investment of financial resources into those projects that are considered to be the most profitable and beneficial to the economy.

- Islamic Banking for Equitable Distribution of Resources: Perhaps the most important objective of Islamic banking is to ensure equitable distribution of income and resources among the participating parties: the bank, the depositors, and the entrepreneurs.

- What Is the Basis of Islamic Banking?

Islamic banking is grounded in the tenets of the Islamic faith as they relate to commercial transactions. The principles of Islamic banking are derived from the Quran, the central religious text of Islam. In Islamic banking, all transactions must comply with Shariah, the legal code of Islam based on the teachings of the Quran. The rules that govern commercial transactions in Islamic banking are referred to as fiqh al-muamalat.

Conventional

and Islamic banking

Conventional banking is essentially based on the

debtor-creditor relationship between the depositors and the bank on the one

hand, and between the borrowers and the bank on the other. Interest is

considered to be the price of credit, reflecting the opportunity cost of money.

Islam, on the other hand, considers a loan to be given or

taken, free of charge, to meet any contingency.

Thus in Islamic Banking, the creditor should not take advantage of the

borrower. When money is lent out on the basis of interest, more often it

happens that it leads to some kind of injustice. The first Islamic principle

underlying such kinds of transactions is that "deal not unjustly, and ye

shall not be dealt with unjustly" [2:279]. Hence, commercial banking in an

Islamic framework is not based on the debtor-creditor relationship.

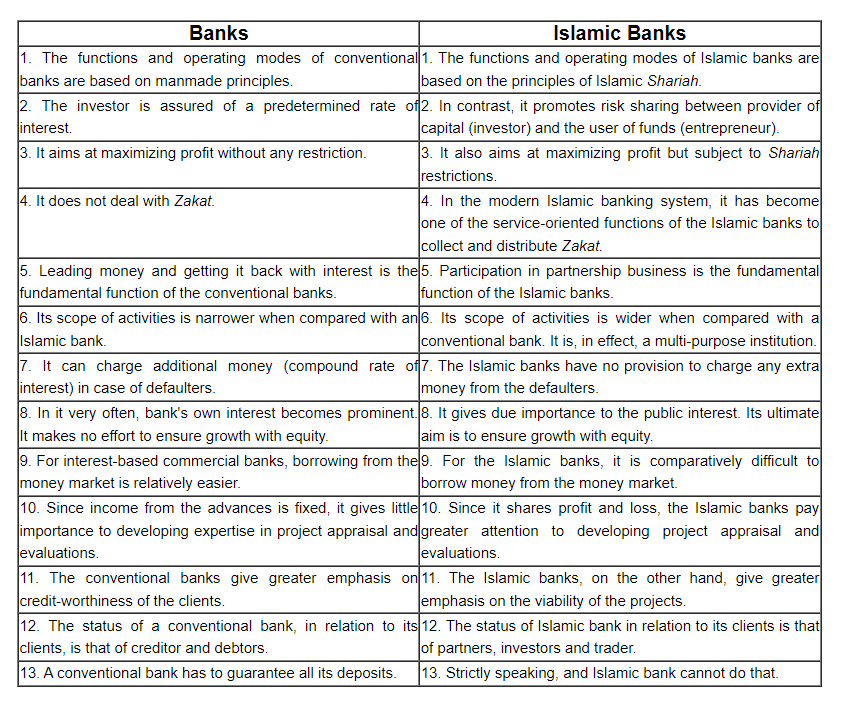

For the interest of the readers, the distinguishing features

of conventional banking and Islamic banking are shown in terms of a box

diagram as shown below:

How Are Conventional and Islamic Banking Different?

One of the primary differences between conventional banking systems and Islamic banking is that Islamic banking prohibits usury and speculation. Shariah strictly prohibits any form of speculation or gambling, which is referred to as Maisie. Shariah also prohibits taking interest on loans. Also, any investments involving items or substances that are forbidden in the Quran—including alcohol, gambling, and pork—are also prohibited. In this way, Islamic banking can be considered a culturally distinct form of ethical investing.

How Do Islamic Banks Make Money?

To earn money without the typical practice of charging

interest, Islamic banks use equity participation systems, which are similar to

profit sharing. Equity participation means if a bank loans money to a business,

the business will pay back the loan without interest and instead give the bank

a share in its profits. If the business defaults or does not earn a profit,

then the bank also does not benefit.

Formation of an Islamic Banking Division:

- a) An Islamic Banking Division has to be set up in the Head Office of the local Bank(s) and in the Country Office (in Bangladesh) in case of foreign Bank(s).

- b) An organizational structure of the division indicating the qualifications and Islamic Banking experiences of the top Executives is to be submitted to the concerned division of Bangladesh Bank.

- c) The responsibilities & duties of the Islamic Banking Division of the concerned Banks

- d) A senior Executive would be the chief of the Islamic Banking Division who shall remain accountable to the CEO. This Division is to be provided with sufficient manpower.

){kind=link}

0 Comments